-----------------------------------------

Series: Beginning Investing (3rd post)

Section: Set Your Goals

-----------------------------------------

Ok, so now have taken the first step on your journey to wealth and financial freedom and you know what you're really worth. And you're ready to start working out your goals and figuring out your financial plan, right?

Wrong.

Before you move on to all the cool 'banker' stuff, it is important to figure out how much you spend. Without this information, all your goals and planning will just remain utopian dreams, your financial plan will not deliver the results you want and you'll eventually be discouraged into giving up the whole thing.

Keep an Expense Diary

The best way to work out your expenses is to maintain a log of your spending every day for at least two to three months, ideally a lot longer. If you're married, have a family or are living with a partner, do this at a household level i.e. maintain a diary of all personal as well as common expenses for the entire family.

Basically, at the end of every day write down your expenses in a little notebook. At the very least, the notebook should have columns for date, expense description and amount (ideally also add columns for expense category and person responsible for the expense) and you should add up the amounts spent every week. It takes 5 mins every day and is well worth the effort.

[When creating categories, make sure you have enough to cover the entire spectrum of expenses in a manner that will allow for meaningful analysis i.e. not too many or too few. I would suggest you set up 7-10 categories as a good number]

Remember to add in credit and debit card expenses as well as spends made through other non-cash means such as food coupons (like Sodexo, Ticket etc.)

For non-monthly outgo such as insurance premia or one-time purchases (like appliances etc) either maintain your diary for a long period and record these as you incur them or make a conservative (implies you should take a pessimistic / worst case) estimate of your annual spends, divide by 12 to reduce it to a monthly value and add it into your expense diary as a 'virtual' expense in an appropriate category.

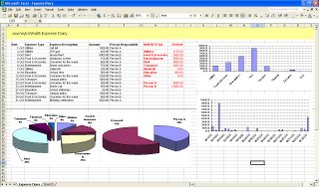

Analyze Your Expenses

If you're somewhat comfortable with spreadsheets, create one or download the one shown here from the Journey to Wealth group to help you create cool graphs and charts that show you just how your expenses break up by category, when the peak spending times are every month, what your average monthly spend is and how your expenses change over time.

If you're somewhat comfortable with spreadsheets, create one or download the one shown here from the Journey to Wealth group to help you create cool graphs and charts that show you just how your expenses break up by category, when the peak spending times are every month, what your average monthly spend is and how your expenses change over time.

Believe me, if you haven't done this before, it's really fun - not to mention it gives a really professional feel to this entire personal finance thing and gives you the satisfaction of getting something done.

If you aren't great with spreadsheets, just manually calculate your average monthly expenses because this is the basic information you need for financial planning.

Testimonial

My wife and I kept such a diary for almost a year. We started because we really needed to find out where our money was going as somehow we never seemed to have any at the end of each month!

It gave us a wealth of information on our spending habits e.g. we discovered we were spending a lot on electricity (the AC was on all the time), telephone bills (we lived away from our parents) and pizzas (that was me) and were able to reduce the spend in those areas significantly. The money we saved went partly into investments and partly into living the good life (a regular Saturday night out). Everybody won!

It is possible you'll read this and think you can already estimate your spends, but that's usually not good enough because you'll invariably miss out some regular (not necessarily monthly) expenses. If you're very sure, keep the diary for a short while but don't skip this step. I can almost guarantee you will be surprised when you maintain this record for a while

***I would like to acknowledge Prasanth for providing some of the material for this post***

Next Post on Beginning Investing: How Much Could You Save?